Mastering Compliance for Fintech: A Founder's Guide to Building an Investor-Ready Asset

Let’s be direct. When a founder hears “compliance,” they think of two things: soul-crushing paperwork and expensive lawyers. It’s seen as a roadblock, a necessary evil you defer until after product-market fit. This is a fatal miscalculation.

Treating compliance for fintech as an afterthought is like building your dream house on a foundation of sand. It might look good for a moment, but it's guaranteed to crumble. For a modern fintech, compliance isn't a checkbox; it's the core engineering that transforms a clever MVP into a high-valuation technical asset that investors will fight for.

Why Compliance Is Your Fintech's Most Valuable Asset

The market data tells the story. While the global fintech market is projected to hit a staggering $460.76 billion next year, the industry faced a major reality check in 2022 when overall funding dropped by 31%.

But here’s the crucial insight: investment in RegTech (the technology that powers compliance) didn't just survive; it thrived, nearly doubling from $11.8 billion to $18.6 billion. The takeaway for founders is clear: investors are tired of hype. They are channeling capital into businesses engineered for longevity. You can dig into more of these fintech industry statistics to understand the implications for your fundraising strategy.

From Cost Center to Technical Moat

As engineers, we are obsessed with building technical moats—the defensible architecture that makes a business difficult to replicate. In fintech, your most powerful moat isn't a slick UI or a clever algorithm. It's your compliance architecture.

A competitor can clone your app's features in a weekend. What they cannot replicate is a deeply embedded, audit-ready compliance framework that has been integral to your product’s DNA from day one.

For a fintech founder, “audit-ready engineering” means building a product where every transaction, user action, and data point is traceable and secure by design. This isn't about passing one audit; it's about engineering a system that is continuously verifiable, building immense trust with regulators, partners, and VCs.

Think of it as the difference between a movie set and a real building. One looks good on camera but falls apart if you lean on it. The other is built to code, designed to withstand hurricanes, and engineered for decades. That is what a robust compliance foundation provides for your startup.

Passing the New Due Diligence Test

The days when VCs and sponsor banks treated compliance as a footnote are over. It is now front and center during technical due diligence. They aren’t just kicking the tires anymore; they are pulling the engine apart to inspect its construction.

Expect to be interrogated with questions like:

Data Governance: How are you protecting customer data to comply with laws like GDPR or various state-level privacy acts? Show me the architecture.

Transaction Monitoring: What happens when a suspicious transaction occurs? What system flags it, and what is the exact process for reporting it under AML rules?

Audit Trails: Can you produce an immutable log of every critical action a specific user took over the last 90 days? Right now?

Arriving with architecturally-sound answers to these questions fundamentally changes the investment conversation. It proves you aren’t just another founder with an idea; you are a serious operator who understands the domain. You have de-risked the investment, which accelerates funding and validates that you are building a real, defensible business.

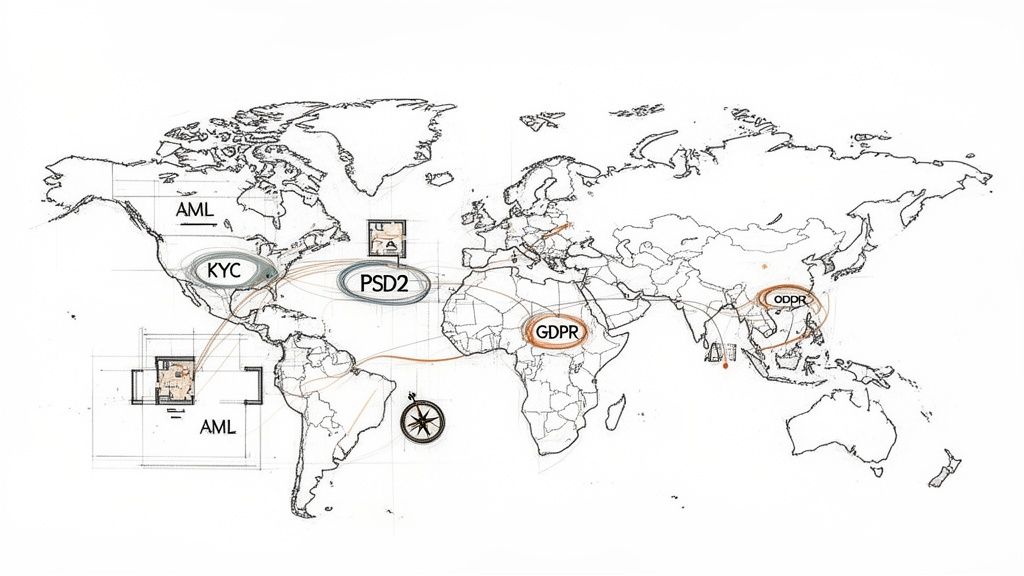

Navigating the Global Fintech Regulatory Maze

For a founder, the global map of regulations can feel like an unreadable ancient script. It's overwhelming. But the secret is this: effective compliance for fintech isn't about memorizing every rule. It's about understanding the core principles that shape the entire system.

You wouldn't build a house without first understanding the local codes for foundations and structural integrity. Similarly, you cannot write a single line of code without knowing the core compliance mandates that will either make or break your product in the market.

The Four Foundational Pillars of Fintech Compliance

Regardless of what you're building—a payment app, a lending platform, or a new investment tool—your entire architecture will rest on four non-negotiable pillars. These aren't just items on a legal checklist; they are deep technical requirements that must be engineered into your product from day one.

Anti-Money Laundering (AML) & Know Your Customer (KYC): This is your front door and your security detail combined. AML dictates that you monitor for, flag, and report suspicious financial behavior. KYC is the process by which you prove your users are who they claim to be. For your tech stack, this means integrating with identity verification services and architecting an intelligent transaction monitoring system that can identify anomalies.

Payment Services Directives (e.g., PSD2): Originating in Europe, its influence is now global. These rules mandate how payment services must operate, requiring Strong Customer Authentication (SCA) and secure open banking APIs. In product terms, this translates to building secure, multi-factor authentication flows and designing an API architecture that is both compliant and bulletproof.

Data Protection & Privacy (e.g., GDPR, CCPA): This governs every single interaction with user data—how you collect it, where you store it, how you use it, and how you protect it. This is not an IT problem; it is a fundamental product architecture challenge that shapes everything from your database schema to your user-facing privacy controls. You must engineer privacy in, not bolt it on later.

Licensing & Registration: Depending on your business model, you will need specific licenses to operate legally. This may seem like a purely legal hurdle, but it carries massive technical implications. Regulators will demand to see specific features, audit trails, and reporting capabilities engineered directly into your product as proof of your operational integrity.

Regional Nuances and Growing Complexity

The rules change depending on your jurisdiction. A significant challenge is navigating the patchwork of Data Privacy Laws Affecting Online Notarization (CCPA, GDPR, State Laws). The U.S., for instance, has no single federal privacy law but rather a complex and growing collection of nearly 20 state-level laws, each with unique requirements.

This complexity is increasing. We are in a technological arms race. Cybercriminals are leveraging AI for sophisticated attacks, while regulators are pushing fintechs to build stronger, more proactive defenses. These 2026 fintech industry predictions make it clear that the ability to rapidly adopt modern regulatory technology (RegTech) is becoming a baseline cost of doing business.

To provide a strategic overview, here is a breakdown of the primary focus for each major region.

Key Fintech Compliance Areas by Region

Region | Primary Regulatory Focus | Key Regulations to Watch |

|---|---|---|

North America | Consumer Protection, State-by-State Privacy, Licensing | CCPA/CPRA (California), Bank Secrecy Act (BSA), State Licensing |

Europe | Data Privacy, Open Banking, Consumer Rights | GDPR, PSD2, MiCA (Markets in Crypto-Assets) |

Asia-Pacific (APAC) | Digital Payments, Data Localization, Cross-Border Data Flow | Varies greatly; PDPA (Singapore), China’s PIPL, India’s DPDP Act |

Latin America (LATAM) | Financial Inclusion, Digital Banking, Payments | Brazil’s LGPD (Data Protection), Open Banking regulations in Brazil & Mexico |

This table only scratches the surface, but it highlights the necessity of tailoring your compliance roadmap to your target markets.

Your compliance strategy must be as agile as your product roadmap. A rule that is gospel in Germany may be entirely different in California. And what is considered best practice today could be a legal mandate tomorrow.

This is why you must build an adaptable architecture, not a rigid one. Instead of hard-coding rules for one jurisdiction, a strategically engineered system uses a flexible rules engine that can be updated as you expand. This is what separates an amateur build from an audit-ready one. It’s how you turn a regulatory headache into a genuine strategic advantage that prepares you for global scale.

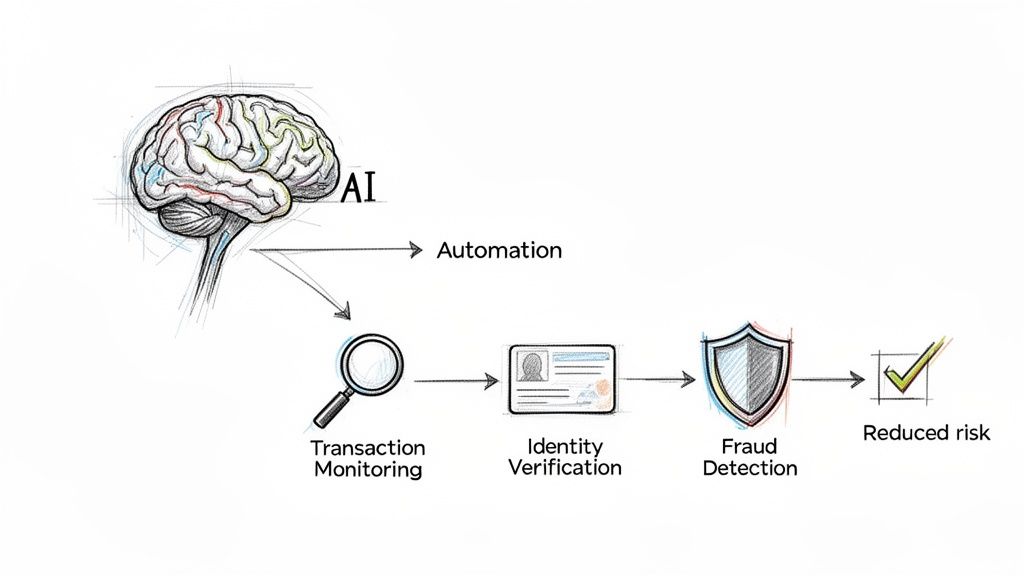

Using AI and Automation for Smarter Compliance

For a startup founder, manual compliance is a losing battle. It's slow, prohibitively expensive, and riddled with human error—three factors that will torpedo an otherwise promising MVP. This is where AI and automation cease to be buzzwords and become the engine for modern, scalable compliance for fintech.

Consider this: a traditional compliance team is like a handful of security guards watching one hundred camera feeds at once. They will spot some obvious problems, but they will miss subtle threats, and they cannot be everywhere at once.

Now, picture an AI system monitoring every single one of those feeds simultaneously. It instantly flags anomalous behavior based on millions of past events and delivers a full report to the team before a critical event occurs. That is the power of a modern RegTech (Regulatory Technology) stack. It transforms compliance from a reactive headache into a proactive, efficient operation that can scale with your growth.

Turning Compliance into a Scalable Operation

For any fintech that wants to be taken seriously by investors, using AI isn't about cutting corners. It's about building a much stronger, more defensible system from day one. Intelligent automation empowers a small, elite team to perform the work that once required an entire floor of analysts. The objective is to automate the predictable so your people can focus on the critical exceptions.

Here is how the most successful startups are executing this:

Automated Transaction Monitoring: AI algorithms can analyze thousands of transactions per second, flagging suspicious patterns that a human would never detect. This is how you fulfill AML duties without grinding your user experience to a halt.

Intelligent Identity Verification: Modern KYC/KYB platforms use AI to verify IDs, detect fraudulent documents, and screen names against global watchlists in an instant. This makes onboarding seamless while hardening your platform against bad actors.

Dynamic Fraud Detection: Forget static, outdated rules. AI models learn from live data to identify and shut down new fraud tactics as they emerge, protecting your users and your capital.

When you engineer these tools into your MVP's architecture from the outset, you are creating a compliance framework that grows with you. You aren’t just shipping a product; you are building an automated, audit-ready asset.

The core principle behind intelligent compliance automation is this: engineer a system that handles 99% of routine work flawlessly. This frees your human experts to analyze the critical 1% that requires their judgment. That is how you build an efficient, high-valuation company.

The Double-Edged Sword of AI Regulation

Here is the strategic catch. As we engineer these powerful AI systems, regulators are looking over our shoulders. For founders, AI is both the solution to compliance and a new source of it. Regulators are now focused on algorithmic bias, the "black box" problem of AI-driven decisions, and data governance.

This means your AI strategy must be built on a rock-solid foundation of responsibility. It is not enough for your model to work—you must be able to explain how it works and prove its fairness. This requires obsessive documentation of your data sources, model training methodologies, and the logic behind its decisions.

For startup builders, the future is defined by this tension. AI provides a massive efficiency boost but also opens a new regulatory front. We are already seeing a heavy focus on AI ethics and mandatory risk assessments for third-party vendors. The market for outsourced AI compliance functions is seeing 57% year-over-year growth. You can get a better sense of where things are headed by reading up on the biggest compliance trends to watch.

Managing Risk from Third-Party AI Vendors

Most startups will not build their own AI compliance models from scratch. You will partner with specialized RegTech vendors. This is the intelligent move, but it introduces third-party risk. Remember, you can outsource a function, but you can never outsource the liability.

If your KYC vendor’s algorithm is found to be biased, or your transaction monitoring partner suffers a data breach, the regulators are coming for you.

This is why your due diligence on AI vendors must be intense. You are not just signing a contract; you are architecting a partnership. You must get past the sales deck and ask the tough, engineer-to-engineer questions:

Model Explainability: Can you provide clear documentation on how your algorithm makes decisions?

Bias Mitigation: What specific steps have you taken to identify and correct for algorithmic bias in your training data and models?

Data Governance: How is our data segregated and secured within your system?

Audit & Access: What kind of audit trails can you provide, and can we access them on demand to satisfy our own regulators?

Choosing a vendor is a major architectural decision. A "black-box" solution is a massive liability. Select partners who are transparent, audit-ready, and understand their role in your broader compliance ecosystem. That is how you build a compliance stack that is not only powerful but, more importantly, defensible.

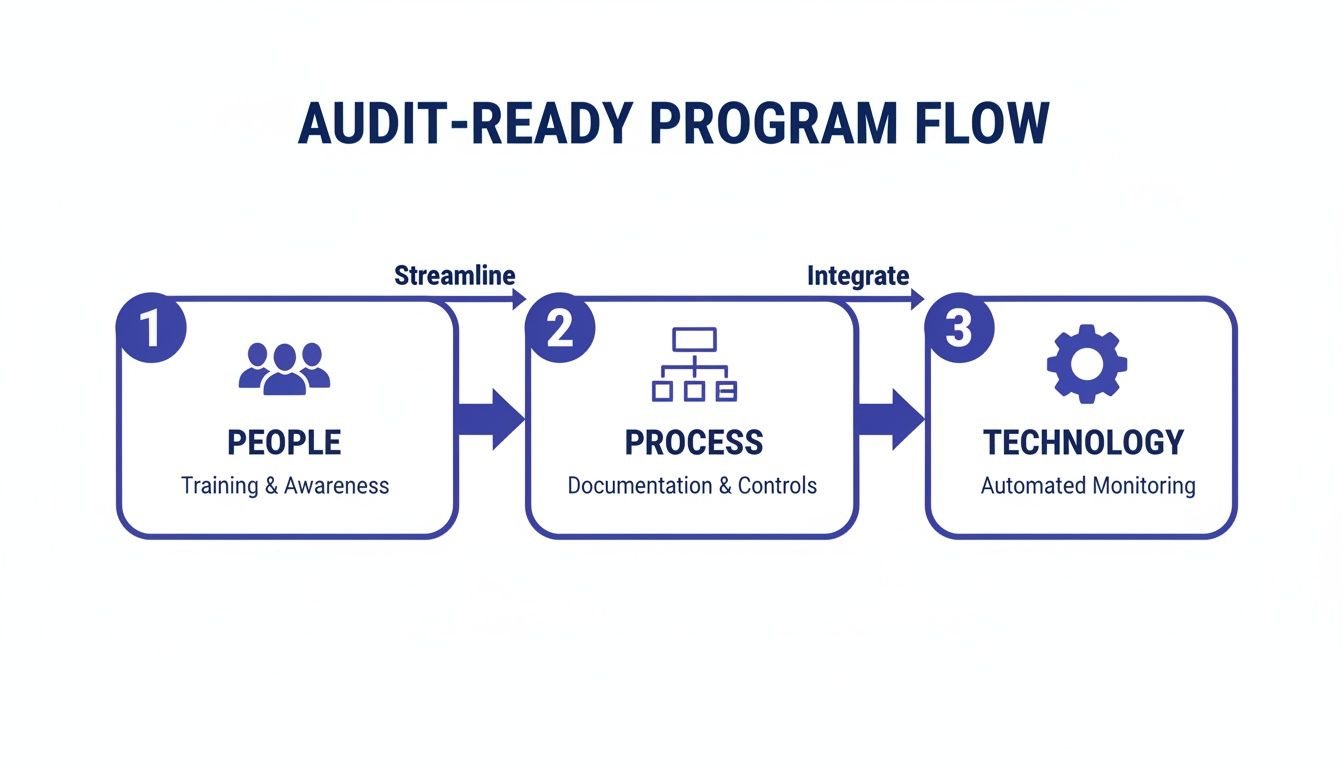

Building Your Audit-Ready Compliance Program

An investor-ready fintech doesn’t just happen. It is engineered. While many founders treat compliance as a fuzzy legal concept, seasoned operators know it is a hard-nosed architectural problem. Building an audit-ready program is about transforming dense regulatory rulebooks into a living system that increases your company's valuation from day one.

A robust compliance program isn’t a dusty binder of policies. It is a system built on three core pillars: the right People, smart Processes, and the right Technology. Neglecting any one of these pillars is a direct path to failure during technical due diligence or a regulatory audit.

The People Pillar: Defining Roles and Responsibilities

First, someone must own this. In a startup, everyone wears multiple hats, but compliance for fintech requires absolute clarity. Ambiguity leads to failure. There must be a designated owner for the compliance strategy, even if it is you, the founder, at the start.

Your goal is to establish a clear line of sight for managing risk. Consider it this way:

A Designated Compliance Lead: This is your point person, even if part-time. They oversee the entire program and report directly to leadership.

Defined Team Responsibilities: Your engineers must understand exactly how their code impacts security. Your support team needs a playbook for handling sensitive data or flagging suspicious activity.

Ongoing Training: Regulations change constantly. Regular, practical training ensures your team remains sharp and understands their duties within the context of your product.

Without clear roles, compliance becomes a game of hot potato. You do not want to be the one left holding it when an auditor arrives.

The Process Pillar: Documenting Workflows for Repeatability

Documented processes transform individual brilliance into a scalable company asset. If your star engineer leaves, their knowledge shouldn't walk out the door with them. The mission is to create workflows so clear a new hire could execute them correctly on their first attempt.

This is where you connect legal requirements to technical actions. An AML rule isn't just a sentence in a document; it’s a trigger for a specific, documented process your technology must execute, every single time.

An audit-ready process is one that is written down, consistently followed, and produces a verifiable output. When a VC or regulator asks, "How do you handle a suspicious activity report?" you shouldn't describe a process—you should show them the documented workflow and the logs to prove it's being followed.

Begin by mapping your core workflows: customer onboarding (KYC), transaction monitoring, data access requests, and incident response. This isn’t just homework for auditors; it’s your roadmap for scaling without breaking. For companies managing infrastructure growth, understanding how processes map to architecture is key. Our guide on cloud migration consulting services explores managing these technical transitions, which follow similar principles of process-first execution.

The Technology Pillar: Selecting a Smart RegTech Stack

Technology is the force multiplier that makes modern compliance function at startup speed. A smart RegTech stack automates manual, soul-crushing tasks, slashes human error, and provides the real-time dashboard needed to see risk before it becomes a crisis. You want tools that are not "black boxes" but transparent partners in your compliance architecture.

Your stack should provide rock-solid audit trails, customizable rules, and intuitive dashboards for monitoring risk in real-time. With new tools, you can even transform tedious checks into efficient workflows. You can learn more about how to use AI for regulatory compliance with AI-Powered Automated Audits to see how it can transform your compliance efforts.

When you integrate these three pillars—empowered People, documented Processes, and intelligent Technology—you stop merely "doing" compliance. You start engineering a real, tangible asset that is ready to withstand the toughest scrutiny from investors and regulators.

Your Phased Roadmap to Fintech Compliance

Building an investable fintech is a marathon, not a sprint. The same is true for your compliance strategy. Attempting to tackle all of compliance for fintech at once is a direct path to burning out and burning through your cash.

A more strategic approach is to phase it out, focusing your precious resources on what truly matters at each stage of your company's lifecycle.

This isn’t about cutting corners—it’s about being strategic. A phased roadmap allows you to build a robust compliance foundation directly into your MVP. From there, you can intelligently layer on more advanced controls as you scale. This keeps you audit-ready without killing your momentum and ensures every bit of engineering effort pushes your valuation forward.

Phase 1: The Investor-Ready MVP

During the MVP stage, your job is twofold: prove your core idea works and demonstrate to investors that you are not reckless with risk. Compliance here is about surgical precision. You're building the non-negotiable foundations to de-risk your venture from day one.

Focus on these priorities:

Core Jurisdictional Analysis: Before writing a single line of code, you must know where you will operate. Engage legal counsel to pinpoint the core licensing, AML/KYC, and data privacy rules for your specific business model in your initial market.

Foundational KYC/AML Controls: You must have a solid process for verifying user identities from the outset. This means selecting and integrating a reputable third-party KYC/AML provider. Attempting to cheap out or hard-code a flimsy solution here creates massive technical debt that will kill a future funding round.

Draft Essential Policies: Work with counsel to draft your foundational documents: your Privacy Policy, Terms of Service, and a high-level AML Policy. These are not legal fluff; they are your public commitments to users and regulators.

At the MVP stage, the goal isn't perfection; it's precision. You must demonstrate a crystal-clear understanding of your primary risks and prove you've engineered credible, foundational controls to manage them. This is how you signal that you are a founder building for the long haul, not just for launch day.

Phase 2: Scaling Post-Launch

Once your MVP has market traction, the compliance game changes entirely. Your risk profile expands with your user base and transaction volume. This phase is about maturing your program from an initial framework into a scalable, data-driven operation that can withstand real scrutiny.

The process below illustrates how the key pillars—People, Process, and Technology—integrate to create a genuinely audit-ready program. This becomes absolutely critical as you begin to scale.

This diagram makes it clear: a strong compliance program is an integrated system. It’s where skilled people follow documented processes using technology that helps them execute their duties.

Here is how to put that system into practice as you grow:

Expand Monitoring Capabilities: The simple transaction flags sufficient for your MVP will no longer suffice. It's time to upgrade your transaction monitoring system to handle more complex, scenario-based rules. You need dashboards that provide a real-time pulse on your key risk indicators.

Prepare for Your First Audit: Begin preparing for an independent audit (like a SOC 2, or PCI DSS if applicable). This means formalizing the processes drafted in Phase 1, gathering verifiable evidence that your controls are working, and ensuring your audit trails are complete and immutable.

Manage Multi-Jurisdictional Complexity: As you explore new markets, your compliance roadmap must evolve. Every new country introduces a new rulebook. Your tech stack needs a flexible rules engine that can adapt to new regulations without requiring a complete rebuild.

To help you stay on track, we’ve created a checklist that breaks down where to focus your limited time and capital at each stage.

Phased Fintech Compliance Implementation Checklist

This table provides a high-level guide to ensure you are deploying resources where they will have the greatest impact as you move from MVP to a scaling company.

Phase | Key Action Items | Primary Goal |

|---|---|---|

Phase 1: MVP | • Identify core jurisdictional risks. | De-risk the venture and build an investor-ready foundation. |

Phase 2: Scaling | • Enhance transaction monitoring with advanced rules. | Mature the compliance program into a scalable, data-driven operation. |

By following a phased roadmap, you transform compliance from an amorphous threat into a manageable, strategic project. You engineer a company that is not just prepared for growth but designed for it—creating a technical asset that is truly audit-ready and built to last.

When to Hire a Fractional CTO or Compliance Expert

As a founder, you are already the lead salesperson, head of product, chief fundraiser, and office therapist. Attempting to also become a part-time lawyer and regulatory expert is not just a poor use of your time—it is a classic startup blunder.

Knowing when to engage specialists isn't an admission of weakness; it is a strategic allocation of capital and focus. You wouldn't draft your own incorporation documents. So why would you attempt to architect your own technical compliance systems when your company's future is on the line? Waiting too long to get this right is how deals die quietly in due diligence.

Key Triggers for Engaging an Expert

Certain moments in your startup's lifecycle are clear signals that it's time to bring in a professional. These are inflection points where your risk profile expands exponentially. If any of these are on your roadmap, the clock is ticking.

Preparing for a Series A Round: Your seed investors likely gave you a pass on a formal compliance program. Your Series A investors will not. They will bring in their own experts to dismantle your tech stack and legal framework. You need an expert on your side of the table, preparing your architecture and your narrative.

Expanding into a Complex Market: Thinking of launching in Europe? Prepare for GDPR and PSD2. Eyeing the U.S. market? You are facing a dizzying patchwork of state-by-state rules. This is no time for guesswork. One wrong architectural choice can lead to massive fines or market exclusion.

Hitting a Transaction Volume Threshold: As your daily or monthly transaction volume climbs, you evolve from a blip on the radar to a very interesting target for regulators and fraudsters. That increased scrutiny demands a compliance architecture that is automated and rock-solid.

Fractional CTO vs. Legal Counsel: The Architect and the Lawyer

It is critical to understand that you are hiring for two distinct, equally vital roles. Confusing them leaves dangerous gaps in your company.

Legal Counsel is your "what" and "why" expert. They interpret dense legal texts, handle license applications, draft policies, and communicate with regulators. They define the rules of the game.

A Fractional CTO is your "how" expert. They take those legal rules and translate them into working technology. They engineer audit-ready systems, select the right RegTech vendors, and ensure your product’s code actually executes what your policies claim. You can learn more about how a virtual CTO can guide your technical roadmap and prepare it for investor scrutiny.

Think of it this way: one expert tells you what the building code requires, and the other designs the blueprints and ensures the structure is strong enough to stand. You need both to build a valuable company that can scale without crumbling under pressure.

Common Questions About Fintech Compliance

Let's cut through the noise. As a founder, you face high-stakes questions about fintech compliance. Getting direct answers is the difference between building a valuable, sellable asset and an MVP that gets crushed during due diligence.

We hear the same questions repeatedly. Here are the direct answers you need to protect your product and position yourself for a high-valuation exit.

How Much Should an Early-Stage Fintech Budget for Compliance?

There is no magic number, but the most common mistake is budgeting zero. A smarter approach is to think in terms of risk mitigation. At the MVP stage, your capital must go into foundational tech—like a solid KYC/AML provider—and sharp legal advice for your initial launch market.

A sound rule of thumb is to allocate 5-10% of your initial tech budget for this. Skimping here isn't saving money; it's creating a mountain of technical debt that is a nightmare to remediate later. It is a red flag that can single-handedly kill a promising investment deal.

Can I Outsource All My Compliance Responsibilities?

You can—and should—outsource compliance functions. You can never outsource the liability. Ultimately, regulators, banking partners, and investors will hold you and your leadership team accountable for any failures.

Using specialized RegTech vendors and expert consultants is an intelligent, efficient strategy. But you, the founder, must own the compliance strategy. Think of it like hiring a contractor to build your house. You own the blueprint and are ultimately responsible for the final structure, even if they swing the hammer.

What Is the Single Biggest Compliance Mistake Fintech Founders Make?

Easy: treating compliance as a problem for "later." The assumption that you can build your entire product and then "bolt on" compliance is a guaranteed recipe for disaster.

This approach invariably leads to painful and expensive architectural teardowns, gaping security holes, and a product that is fundamentally un-investable. Audit-ready engineering must be part of your MVP’s DNA from day one. It is not a feature; it is the foundation.

How Does Compliance Differ for B2B vs B2C Fintech?

While core principles like data privacy and anti-money laundering apply to both, the strategic focus shifts dramatically. B2C fintechs are under a microscope for consumer protection, performing KYC on a high volume of individuals, and ensuring marketing is transparent and not misleading.

B2B fintechs, on the other hand, wrestle with more complex onboarding. You aren't just verifying a person; you are dealing with KYB (Know Your Business). This involves deep dives into corporate structures, managing the risk inherited from your clients' own vendors, and engineering rock-solid data segregation to keep one corporate customer's information completely isolated from another's.

At Buttercloud, we don't just build apps; we engineer high-valuation technical assets. We partner with founders to embed audit-ready compliance into their architecture from day one, transforming regulatory hurdles into a competitive moat. Build your investor-ready MVP with us at https://www.buttercloud.com.